If you are living with a chronic condition such as HIV, diabetes, high cholesterol, hypertension or asthma, you may have wondered whether you can still get life insurance, and how it differs from critical illness or dread disease cover. These products sound similar but serve very different purposes. Understanding the difference is essential when planning for long-term financial protection.

Chronic life cover is a life insurance product designed specifically for people living with chronic conditions. Traditionally, having a condition like HIV, diabetes or hypertension made it difficult or expensive to get life cover.

This is where Dis-Chem Life’s Chronic life cover changes that. Our chronic life cover offers up to R10 million (risk profile dependent) in cover for people managing their chronic condition including:

What makes this product unique is that it rewards healthy behaviour. Premiums can be reduced by up to 60% from day one, based on premium comparisons done on a like for like most major insurers on 1 January 2025, and your cover can increase in line with your annual health management.

By staying on top of your chronic medication by refilling your script at Dis-Chem and attending regular health checks at Dis-Chem, you are rewarded with better rates and improved benefits.

Chronic life cover includes:

This gives you comprehensive protection even if you have a pre-existing condition.

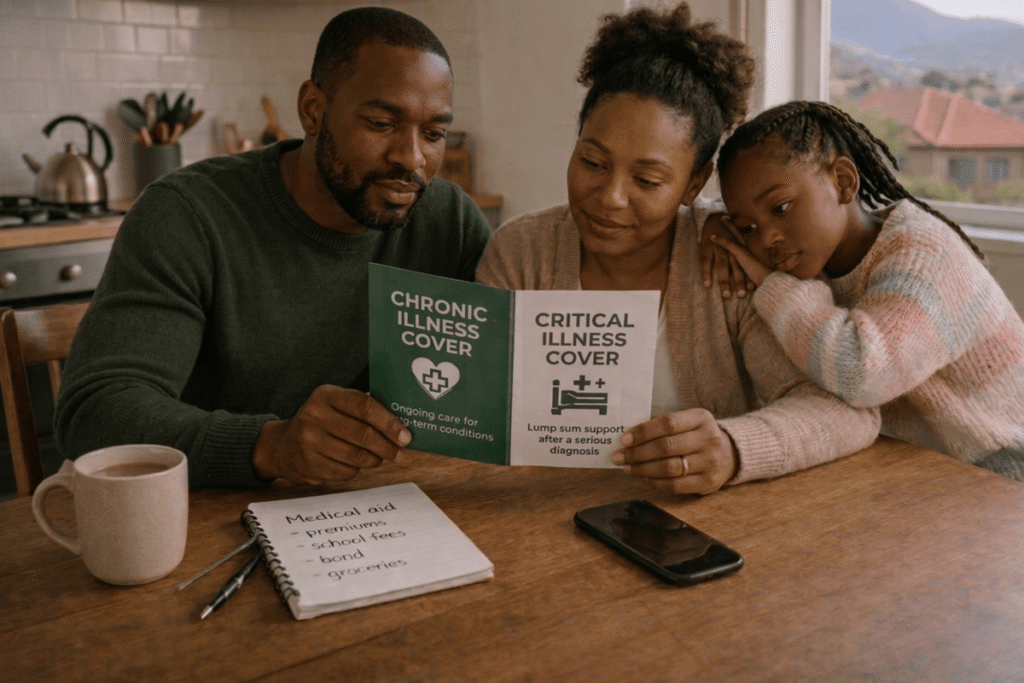

This is not a medical aid benefit. It is a standalone life insurance product that pays out upon death, disability or diagnosis of a specified serious illness.

Critical illness cover, also known as dread disease cover, provides a once-off lump sum payout after diagnosis of a specified serious condition, such as:

In South Africa, the terms “critical illness cover” and “dread disease cover” are used interchangeably. They refer to the same product.

Unlike medical aid, the payout is not limited to medical expenses. It can be used for:

This flexibility allows families to manage the broader financial constraints of a serious illness. Medical aid supports the treatment plan whereas critical illness cover supports your life plan.

Chronic Life Cover

Thabo is a 42-year-old father of two living with HIV. He has been on ARVs for years and manages his condition well. But because of his status, he was previously declined for life insurance by two providers. With Chronic Life Cover through Dis-Chem Life, Thabo is now covered for up to R5 million, with reduced premiums because he stays on top of his medication and attends annual health checks. If something happens to Thabo, his family is financially protected.

Critical Illness Cover (Dread Disease Cover)

Naledi is a 38-year-old teacher and the primary breadwinner in her household. She is diagnosed with stage 2 breast cancer. Her medical aid covers the oncology treatment, surgery and follow-up care. But as medical technology improves, surviving does not automatically mean returning to normal life financially. Six months into recovery, the financial picture looks very different:

A critical illness payout of R500,000 would have covered income replacement, kept the family out of debt and allowed Naledi to focus on recovery without the added stress of financial survival.

The numbers are significant and According to Thembisa modelling data published in March 2025, over 8 million South Africans are living with HIV.* Research published in the South African Medical Journal found that approximately 37% of South African adults have hypertension, with around 7.1 million cases likely undiagnosed, while an estimated 2.7 million cases of diabetes remain undiagnosed.** These are not rare conditions. They affect millions of working-age adults and their families.

For many South Africans, getting affordable life insurance has historically been a challenge. Many traditional insurers either decline applications outright or charge significantly higher premiums based on a chronic diagnosis alone.

Chronic Life Cover addresses this gap. It recognises that a well-managed chronic condition does not define your risk in the same way it once did. If you are adherent to your medication, manage your health proactively and attend regular check-ups, your premiums should reflect that.

This means that managing your health is not just good for your well-being but also good for your wallet too.

Planning for illness is not only about covering medical costs. It is about protecting your financial future and the people who depend on you.

If you are living with a chronic condition, you deserve the same access to life insurance as anyone else. Chronic life cover makes that possible, while rewarding you for managing your health better.

If you are concerned about what would happen financially if you were diagnosed with a serious illness like cancer, heart attack or stroke, Critical illness cover (dread disease cover) provides the safety net your medical aid can’t.

In simple terms:

By understanding the difference between Chronic life cover and critical illness cover (dread disease cover), you can make informed decisions that support both your health and your long-term financial well-being.

Chronic Life Cover is a life insurance product designed for people living with chronic conditions such as HIV, diabetes, hypertension, high cholesterol and asthma. It provides access to life, disability and critical illness cover with reduced premiums for people who manage their health proactively.

Chronic Life Cover is life insurance for people with chronic conditions. It pays out on death, disability or serious illness. Critical illness cover (also called dread disease cover) is a specific benefit that pays a lump sum upon diagnosis of a serious condition like cancer or heart attack. With Dis-Chem Life, critical illness cover is included as part of Chronic Life Cover.

Yes. In South Africa, these terms are used interchangeably. Both refer to a policy that pays a lump sum upon diagnosis of a specified serious illness

Yes. Dis-Chem Life’s Chronic Life Cover is specifically designed for people living with chronic conditions including HIV, diabetes, hypertension, high cholesterol and asthma. You can get cover of up to R10 million.

Dis-Chem Life offers reduced premium rates of up to 60% from day one. Your cover can increase in line with your annual health management. By staying on your chronic medication and attending health checks at Dis-Chem, you benefit from better rates and improved cover.

Visit www.dischemlife.co.za for a quote and one of our agents will call you back. Alternatively, you can visit one of our selected Dis-Chem stores and speak to an advisor in person.

T&Cs apply. Dis-Chem Life is an authorised financial services provider – FSP 50594. Products are underwritten by Guardrisk Life Limited, an authorised financial services provider (FSP No 76) and a licensed life insurer. Nothing in this article should be interpreted or regarded as providing financial advice.